Did the S&P 500’s downgrade of the U.S. government’s credit rating change how investors view the risk of default in the United States? Better still, what events during the past several years coincide with changes in the risk of the U.S. government defaulting on the debt it issues?

We can answer these questions by seeing how the spreads of Credit Default Swaps (CDS) – the special insurance policies that investors in debt securities can buy that pay out in the event the borrower defaults on their owed debts, have changed over time. Because the costs (or spreads) of these insurance policies are dependent upon the likelihood of default, we can correlate changes in their level over time with the events that could drive the observed changes.

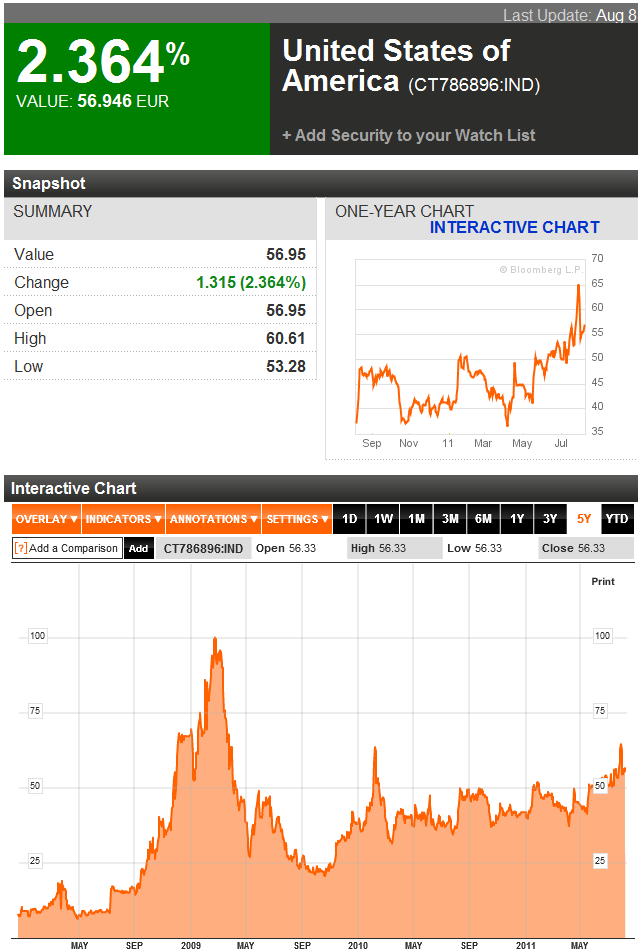

The chart below shows the risk of the U.S. defaulting on its 10-Year Treasury as measured by CDS spreads from 14 December 2007 through 8 August 2011, an interactive version of which is available from Bloomberg:

We’ll next go through the major gyrations shown in the chart above, providing a timeline of the major events that could influence the perception of the risk of a U.S. default from the end of 2007 through the aftermath of S&P’s credit rating downgrade of the creditworthiness of the U.S. government.

| Significant Events Coinciding with Changes in U.S. Default Risk | |||

|---|---|---|---|

| Starting Date | Ending Date | CDS Direction: Range | Milestone |

| Before | 22 Feb 2008 | Flat: Between 6 and 10 | Typical Level of U.S. Credit Default Swap (CDS) Spreads (aka “default risk”) in “Pre-Financial Crisis” Period |

| 22 Feb 2008 | 1 May 2008 | Increase: From 11 to 18 | Subprime Lending Crisis begins as banks act to bail out bond insurer Ambac. Bear Sterns collapses and is acquired for pennies on the dollar by JPMorgan. |

| 1 May 2008 | 8 Jul 2008 | Decline, Flat: Fall to Between 6 and 9 | Post-Subprime Crisis spike returns to typical pre-crisis CDS spreads. |

| 8 Jul 2008 | 5 Sep 2008 | Increase: From 9 to 16 | IndyMac bank fails. Fannie Mae and Freddie Mac (both government-supported enterprises) both increasingly seen at risk. Both are seized by federal government on 7 September 2008. |

| 5 Sep 2008 | 24 Feb 2009 | Increase: From 16 to 100 | U.S. Financial System Crisis explodes. CDS Spreads peak at 100 on 24 February 2009. |

| 24 Feb 2009 | 30 Oct 2009 | Decline: From 100 to 21 | First phase of financial system crisis abates. U.S. Treasury issues “Next Phase” report in September 2009, which anticipates how emergency financial support from the federal government to the financial industry will wind down. |

| 30 Oct 2009 | 8 Feb 2010 | Increase: From 22 to 47 | Second phase of financial system crisis begins with failure of Citigroup, which declares bankruptcy on 1 November 2009. The move forces U.S. government to write off $2.3 billion in TARP bailout money. |

| 8 Feb 2010 | 16 Mar 2010 | Decline: From 47 to 31 | Secondary U.S. financial system crisis abates. Federal Reserve begins to unwind emergency measures. |

| 16 Mar 2010 | 4 Aug 2010 | Increase: From 31 to 40 | U.S. default risk increases as U.S. new government debt issues continue to flood the markets in record quantities, with debt buyers beginning to balk at amount of U.S. Treasuries being issued to support government spending, as U.S. Congress controlled by Democratic Party declines to pass budget for federal government. |

| 4 Aug 2010 | 12 Oct 2010 | Increase: From 40 to 50 | A second step upward in U.S. default risk as concerns begin to grow as U.S. nears national debt ceiling with no action being taken by U.S. Congress, which is fully controlled by Democratic party. |

| 12 Oct 2010 | 14 Jan 2011 | Decrease: From 44 to 36 | Likelihood of Republican party winning U.S. Congress pushes default risk downward, as “Tea Party” candidate campaigns focusing on reducing excessive government spending prove popular. After dipping to low of 36 ahead of 2010 election, default risk rises slightly as Democratic party retains control of U.S. Senate, limiting potential for bringing federal spending into control. |

| 14 Jan 2011 | 31 Jan 2011 | Increase: From 48 to 52 | Short term spike as President Obama releases Fiscal Year 2012 budget, demonstrating intent to continue and increase excessive levels of government spending, with no plan to reduce it through remainder of his first term. |

| 31 Jan 2011 | 6 Apr 2011 | Decrease: From 52 to 36 | Decline in default risk as Republican party controlled House of Representatives passes a budget blueprint developed by new House budget committee chairman Representative Paul Ryan designed to bring federal spending back under control and sets to work on creating budget legislation based upon it. |

| 6 Apr 2011 | 18 Apr 2011 | Increase: From 36 to 50 | Spike in U.S. default risk as President Obama sketches out a “second” budget in national speech on 13 April 2011, which continues excessive levels of government spending while also seeking to reduce annual budget deficit by increasing taxes that are unlikely to be supported by Republican-controlled House of Representatives. |

| 18 Apr 2011 | 17 May 2011 | Decrease: From 50 to 41 | Decline in default risk as “Ryan” deficit reduction plan passes U.S. House of Representatives. |

| 17 May 2011 | 1 Jun 2011 | Increase: From 41 to 51 | U.S. Senate rejects “Ryan Plan” without developing any alternative of its own. U.S. reaches $14.3 trillion debt limit. |

| 1 Jun 2011 | 13 Jul 2011 | Flat: Between 50 and 54 | Range of volatility in CDS spreads while deficit reduction/national debt limit increase negotiations are ongoing. |

| 13 Jul 2011 | 18 Jul 2011 | Increase: From 50 to 56 | Short term spike in default risk as President Obama storms out of national debt limit negotiations. |

| 18 Jul 2011 | 22 Jul 2011 | Decrease: From 56 to 53 | Obama returns to the table in secret negotiations at the White House to resume debt limit talks. |

| 22 Jul 2011 | 28 Jul 2011 | Increase: From 53 to 64 | Short term spike as Speaker John Boehner withdraws from national debt limit talks in face of Obama/Senate Democrats refusal to consider any spending cuts, insisting instead upon imposing massive tax hikes and continuing unsustainable levels of spending, as uncertainty rises as its unclear that “Tea Party” representatives will accept higher spending levels in Boehner’s scaled back compromise proposal. |

| 28 Jul 2011 | 2 Aug 2011 | Decrease: From 64 to 54 | Boehner offers new scaled-back deficit reduction/higher national debt limit plan, which passes the U.S. House on 29 July 2011. Two part spending reduction plan reduces immediate risk of default, which results in lowering CDS spreads to pre-spike level. Deficit reduction/national debt limit increase plan signed into law by President Obama on 2 August 2011. |

| 2 Aug 2011 | 8 Aug 2011 | Flat: Between 54 and 57 | U.S. default risk, as measured by 10 Year Treasury CDS spreads essentially holds level within a narrow band of volatility, even though S&P issues downgrade to rating of U.S. debt from AAA to AA+ on 5 August 2011. Downgrade has very little no effect on U.S. default risk (debt ratings only *confirm* status of U.S. financial situation – they don’t actually change it!) |

And that’s how the U.S. government got from having an “almost zero” risk of defaulting on its debt payments to where we are today!![]()

|

|

|

|