If the United States were make a real effort to run a budget surplus for the sake of cutting its national debt burden in half by the year 2050, how big would those budget surpluses have to be?

The Economist answers the question for the U.S. and 25 other nations in chart form:

The Economist’s Ryan Avent explains:

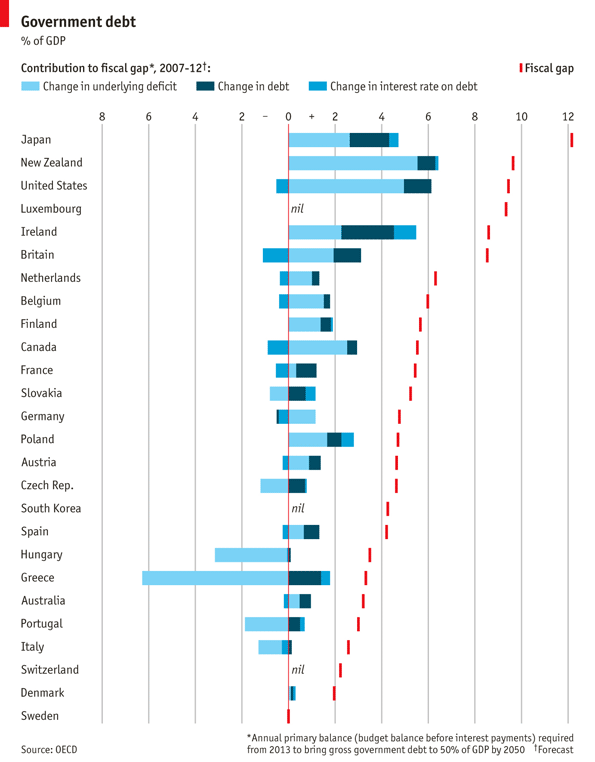

Let me explain what you’re looking at here. We’ve charted a fiscal gap, which is defined as the budget surplus (net of interest) that a government would need to run from 2013 on if it wanted to reduce its sovereign-debt load to 50% of GDP by 2050.

Focusing on the U.S., whose national debt burden (the ratio of its total public debt outstanding to the nation’s GDP), is just over 100%:

So take America (please!). Currently its gross debt-to-GDP ratio is a bit over 100%. In order to reduce its debt load, as a share of GDP, by half by the year 2050, the government would need to average a budget surplus of nearly 10% of GDP (before taking into account interest payments). That’s a much bigger surplus than it would have needed to run had debt remained stable through the Great Recession; gross debt-to-GDP was just 65% in 2007 (it was 57% in 2000, since you ask).

He goes on to identify the factors that caused the U.S.’ fiscal gap to increase, and compares it with the plight of other nations that have seen similar increases in recent years.

For America, the increase in this fiscal gap is mostly due to the substantial deficits run over the past 5 years. Elsewhere, the substantial rise in the debt stock is to blame (like in Ireland, where the government took on massive bank debts). In a handful of countries, a big rise in interest rates is to blame, whereas in Britain and America interest rates have actually shrunk the gap a bit.

So there’s the silver lining: It’s not as bad as it could be! Of course, we should probably recognize that other nations’ pain has been to the U.S.’ gain where investors seeking safer havens have been concerned. In a really perverse way, it is to the government’s current advantage for other nations to go through their own debt-driven crises, because that makes our own debt-driven crisis better.

|

Featured Image:

Courtesy of The Zeitgeist Movement Media Project |

|

|

|

|